Top 3 factors that determine which investment strategy is right for you

When it comes to investing, every investor has their own personal tastes and preferences. Investors approaching retirement tend to be more conservative and prefer strategies with lower risks while young working adults usually have a higher risk appetite and are willing to stomach some volatility in exchange for higher returns. Whichever strategy you choose, it is important that you are comfortable with the risk it entails so that you are able to stick to your strategy and avoid making emotional decisions.

There are three key factors that determine which investment strategy is right for you.

-

Risk tolerance

-

Expected returns

-

Effort required to implement the strategy

Risk tolerance

The first factor is your risk tolerance which is the amount of risk you are willing to take on in exchange for a return on your investment. Generally, investment strategies with higher risks should be rewarded with higher returns. You should choose an investment strategy with a target risk that you are comfortable with and will not cause you to lose sleep at night.

Many investors are often attracted to the high returns from an investment strategy. However when markets get volatile, and they start seeing huge fluctuations in their portfolio’s value, they are unable to stick to the plan and get shaken out of their positions. They end up panic selling and crystalizing huge losses on their portfolio.

One way you can measure the risk of your strategy is to backtest your investment strategy and find out the maximum drawdown of your strategy.

The maximum drawdown tells us what is the maximum amount of money you can lose on your portfolio during a crisis. For example, during the 2008 crisis, the S&P 500 lost 55% from it’s peak value in October 2007 to March 2009.

You need to ask yourself how much are you prepared to lose if markets were to crash and are you willing to stay the course. Retirees who need to gradually withdraw their funds for their daily expenses should only invest a small percentage of their wealth that they can afford to lose. Young working adults on the other hand should take on more risk because they have time on their side to ride out any market crashes.

For me personally at 30 years old, I’m comfortable with a 50% drawdown on my portfolio if a black swan event such as the 2008 global financial crisis were to happen again. When I’m 50 years old, I would be comfortable with a 30% drawdown on my portfolio.

Expected Returns

The second factor that determines your investment strategy is expected returns. How quickly do you need your money to grow to achieve your financial goals?

The math shows that if you save $50 a day for 20 years at a 10% rate of return, you will end up with over a million dollars. However, if your investment strategy is expected to make 5% a year, it is extremely unlikely that you will hit a million dollars at the same saving rate. This could mean being able to free yourself from the corporate rat race a few years earlier and being able to provide a significantly higher standard of living for your loved ones.

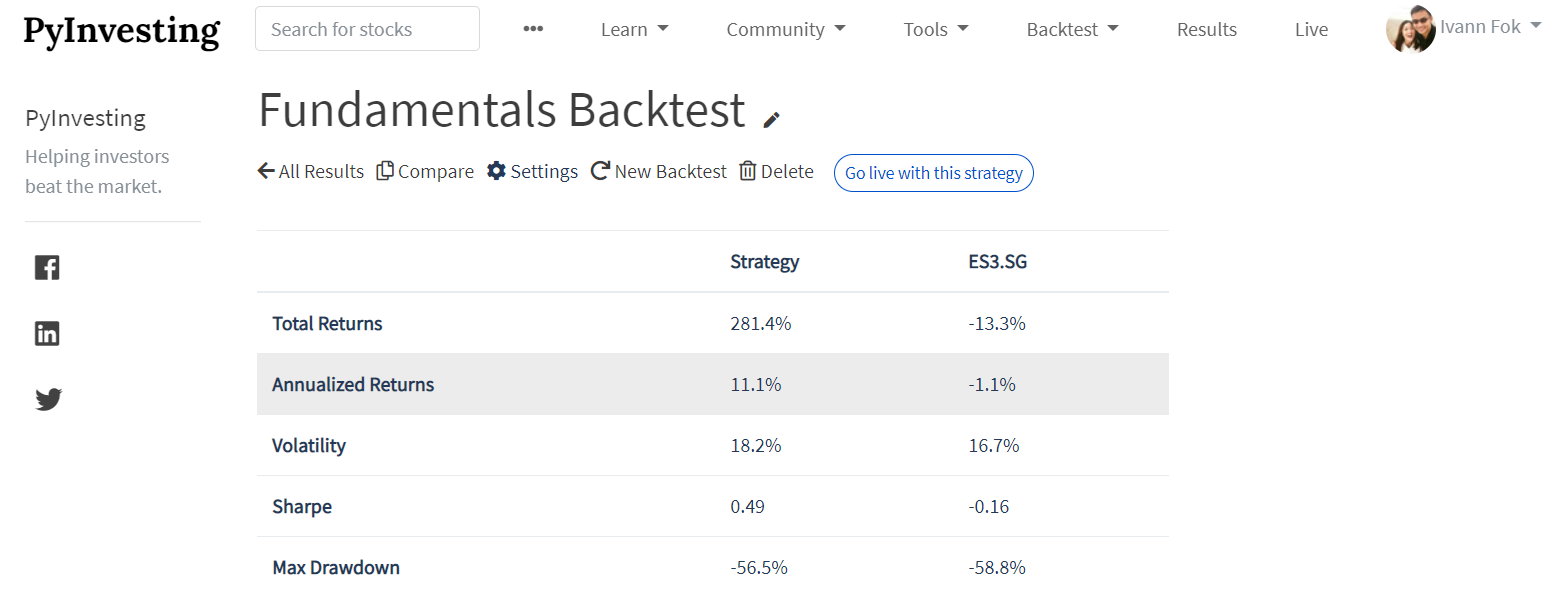

You can measure the expected returns of your strategy by backtesting it using historical prices and calculating the annualized returns. Check out this tutorial video below to find out how you can analyze the performance of your investment strategy.

Once you get the annualized returns from your backtested investment strategy as shown below, you can plug that value into the CPF retirement calculator to find out whether you are able to hit your financial goals.

Effort Required

The third factor is how much effort you are willing to spend on managing your investments. Some strategies require less work to maintain than others and would appeal to more hands off investors. It is important to choose a strategy that fits the amount of effort you are willing to commit to implement the strategy. This is because if you choose a strategy that requires more time to implement than you are willing to commit, you could end up finding it a chore to manage your portfolio and eventually give up on following your strategy.

For investors who are not willing to spend a lot of time managing their portfolio, long term strategies such as the Ray Dalio all weather strategy, would be a great fit. This strategy involves allocating a fixed percentage of your portfolio in specific asset classes such as stocks, bonds, REITs and commodities and rebalancing the portfolio once a year to the portfolio’s target allocation.

Investors that are able to spend more time managing their portfolios are able to adopt more active strategies such as a moving average strategy where they monitor their positions on a weekly basis. Note that actively monitoring your positions does not necessarily mean you are trading every week. The investor could simply be frequently checking each position more frequently but only opportunistically trading a small number of stocks in the portfolio if they change their buy or sell conviction.

Backtest your investment strategy

When choosing our investment strategy, it is important to consider our risk tolerance, our expected return and the amount of effort we are willing to spend on managing our portfolio. Having the right investment strategy will allow us to stay invested even when markets are volatile and help us achieve our financial goals.

Backtesting your investment strategy will allow you to estimate the strategies expected risk and return, and understand the amount of effort required to manage your portfolio. While most portfolio backtesting methods involve expertise in programming and statistics, we can use platforms such as PyInvesting.com to simply fill in a form and create a backtest. The website will run your investment strategy using live prices and send you an email with the orders you need to trade on your personal account.

Stay the course, and may the odds be in your favor.